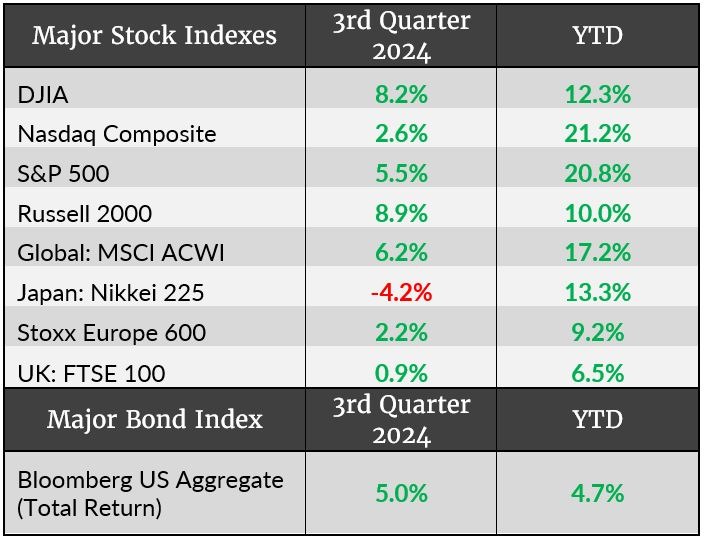

There was a lot of green on the scoreboard last quarter. It was an action-filled quarter in the financial markets underneath the seemingly tranquil green numbers on this page. Although there’s plenty of action in any quarter, it was particularly interesting for a few reasons. We consider three developments most noteworthy.

The Federal Reserve dropped interest rates for the first time since 2020. Meanwhile, the U.S. economy enjoyed another recession-free quarter despite some indicators suggesting a recession should have happened by now. Additionally, broad U.S. stock indexes stumbled during the dog days of summer, but they recovered quickly and set new all-time highs in September.

A Turning Point in Short-term Interest Rates

The interest rate landscape affects all financial markets directly or indirectly. The Federal Reserve’s (Fed’s) September 18 reduction in short-term interest rates marked a turning point in the interest rate cycle. It was also a milestone event because analysts and investors study the Fed’s interest rate posture to glean insight into the broader economy’s standing.

The lowering of interest rates was highly anticipated. Uncertain until the day of the announcement, however, was the amount of the Fed’s trim. With both the jobs picture and inflation softening, the central bank lowered its key overnight borrowing rate by the bigger of the two choices: 50 basis points (0.50%) as opposed to 25 basis points (0.25%). The move takes the federal funds rate range from 5.25%-5.50% to 4.75%-5.00%.

The decision to trim rates by the larger of those two increments implied that Fed officials seem to be gazing more into the economy’s employment situation and away from the inflation battleground, which arguably is a battle already being won. Annual inflation is easing, from an over four-decade high of 9.1% in June 2022 to 2.5% in August of this year.

The Fed is now trying to prevent past interest rate increases, which last year took borrowing costs to a two-decade high, from further weakening the U.S. labor market. When questioned about whether the Fed is behind the curve, Powell said, “We don’t think we’re behind – we think this is timely. But I think you can take this as a sign of our commitment not to get behind.”

Historically, rate cuts are meant to stimulate economic activity by lowering the cost of borrowing for consumers and businesses. The market’s concern is that the larger 0.50% cut might mean the Fed sees a potential slowdown in economic growth, which may have been the result of tightening financial conditions over the past few years.

If interest rates keep falling as expected then conservative investors could see their portfolios’ income lessen, all else being equal. Many of us were enjoying 5% rates on money markets, CDs, and other conservative investments without much thought required. Folks spoiled by relatively high interest rates on conservative investments recently might rethink an appropriate risk-reward balance for total return potential.

An Un-inverted Yield Curve

A bond market indicator that’s often cited as a recession predictor is no longer indicating a high potential for an economic downturn. Since mid-2022, the yield of the 2-year U.S. Treasury note had been higher than that of the 10-year Treasury. This is a rare occurrence known as a yield curve inversion. Longer-dated bonds normally provide higher yields than shorter-dated bonds, but it’s the opposite during inverted periods. These inverted periods historically have predicted recessions.

On September 4, the 2-year yield crossed back below the 10-year yield, and it has since stayed there. September 30’s closing 2-year yield was 3.65%, and the 10-year yield was 3.80%. Short-dated bonds’ yields fell fast as the bond market anticipated the Fed’s action, thus normalizing the yield curve. The yield curve was inverted for a record 793 days, but a recession didn’t occur like expected according to historical precedent.

Did the inverted yield curve “cry wolf”? For now, the answer is yes. However, as James Mackintosh wrote for the Wall Street Journal on September 11, “If [the Fed’s] rate cuts are purely because inflation has dropped back close to target, that is the ideal of a soft landing for the economy, and absolutely not a sign of imminent recession. But for most of modern history, deep rate cuts by the Fed have been a sign that the country is about to plunge into recession, or is already in one that economists missed.”

What does this mean for us? We believe investors should be careful about reading too much into the yield curve. Currently it tells us what we already know: that the Fed has and will likely continue to cut rates. But it doesn’t tell us what we really want to know: whether a recession is imminent. Therefore, as always, it’s prudent to stick to a long-term investment strategy based on your unique goals and objectives.

A Resilient Stock Market

Major U.S. stock indexes enjoyed another great quarter, but it wasn’t a smooth ride higher. Early August saw an 8% decline in the S&P 500 in just four days, volatility not felt in months. Yet by August 19, the market had recovered and stabilized above the August 1 high. The S&P 500 and Dow Jones Industrial Average made new record closing highs on September 30 to bid the quarter a poetic farewell.

Granted, there probably will be more volatility between now and the end of the year. “What matters is how you respond,” Liz Ann Sonders of Charles Schwab reminds us in a September 16 article. “If you’ve built a portfolio that is directly tied to your time horizon and risk tolerance when markets are calm, then a surge in turbulence may not leave you shaken. Good planning, and discipline along the way, is like a pre-emptive dose of Dramamine – it can help neutralize some of the nausea before the turbulence hits.”

Our team echoes Liz Ann’s sentiment. Our aim is to help you feel comfortable with your investment portfolio, designing it to meet your objectives over time. Please let us know how we can be helpful in this way.