This is the biggest election year in world history. Seventy-six countries – home to roughly 4.4 billion people – will hold political contests in 2024. The most watched race will be for U.S. President. The composition and control of Congress is another aspect of this year’s election cycle that deserves attention. What does history imply about the stock market in the context of U.S. elections and political party leadership?

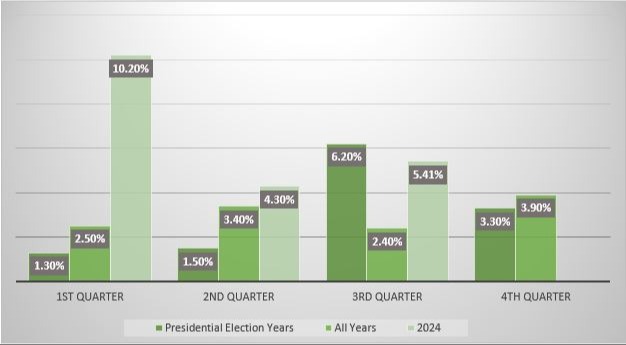

Historically, stocks have risen 11.6% during presidential election years since 1926, slightly better than the market’s average 10.3% return in all years. Drilling down further, stocks tend to follow a pattern during presidential election years: sluggish in the first half, followed by a big second half. The third quarter has delivered the strongest returns, with an average return of 6.2%.

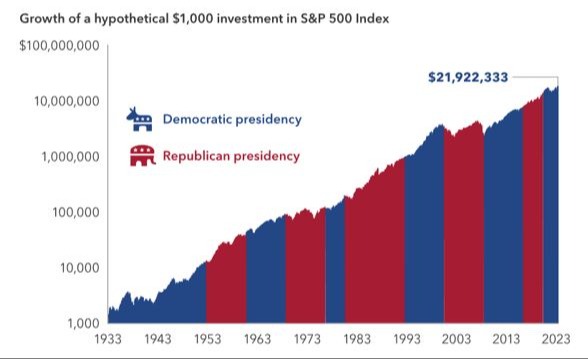

There is often some anxiety about how a president’s four-year term might impact the stock market. We believe that anxiety is for naught. Seeing the big picture can help us to stay focused on our long-term investment goals. Over the past 92 years, the S&P 500 Index has delivered positive performance 73% of the time and has averaged an annual total return of 11.54%. Despite the constant headlines around elections, investors should remain focused on factors such as economic growth, interest rates, inflation, and corporate earnings when making portfolio decisions.

Along with the headline Presidential race, one-third of the seats in the U.S. Senate (currently under narrow Democratic control) and all 435 seats in the U.S. House of Representatives (currently under narrow Republican control) are also on the ballot this fall. Here, too, a small margin may determine control beginning in 2025, with winners in many closely contested seats difficult to predict. It is conceivable that the election outcome could result in one-party control of both houses of Congress and the Presidency, or a split between the two parties, as exists today.

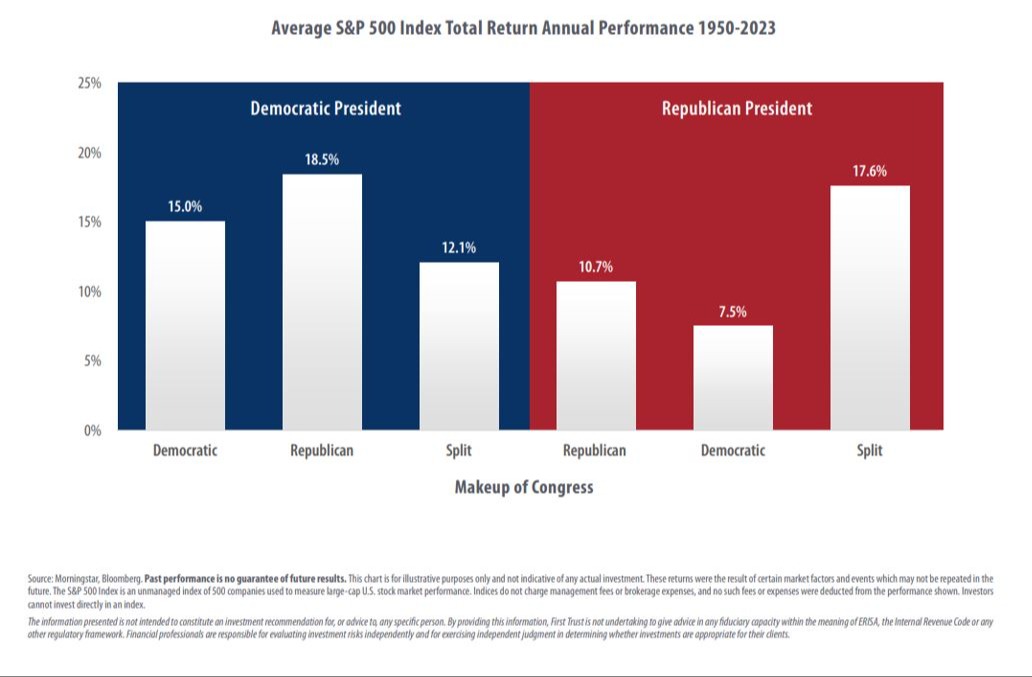

When one party controls the White House and has majorities in the Senate and House of Representatives, the potential to pass meaningful legislative changes is greater. Divided government, on the other hand, usually makes it harder to push through sweeping changes. A study by U.S. Bank reveals there are insignificant return variances in the 3 months following an election compared to any other 3-month period from 1948 – 2023, regardless of political control. However, reviewing S&P 500 annual average returns from 1950 – 2023 the index outperformed with a divided government.

In addition to economic issues, many others will come up for debate as the campaign season unfolds. Immigration, abortion, climate change, and global trade will certainly be among them. In the realm of international relations, we will hear arguments about the wars in Ukraine and the Middle East, along with rising tensions between the U.S. and other parts of the world.

All of this may result in market volatility, particularly as we get closer to November 5. Markets do not like uncertainty, and this election is likely to produce a lot of it. But there is one important point to keep in mind: Over the long term, going as far back as the 1930s, U.S. stocks have nearly always been higher at the end of a president’s term in office than they were at the beginning, regardless of party affiliation.

The bottom line is not to let politics derail your investment plans! We believe that investment decisions should be based on longer‑term fundamentals and your personal financial planning objectives, not near‑term political outcomes.