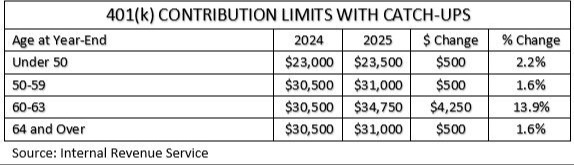

Most workers will be allowed to contribute up to $23,500 to their 401(k)s and similar workplace retirement plans in 2025, up $500 from 2024. Workers 50 to 59, or 64 and older, can make an additional catch-up contribution of up to $7,500, the same as 2024.

The most significant change, called the super catch-up, is for those turning 60 to 63. Through Congress’ SECURE 2.0 modifications effective starting in 2025, a higher catch-up contribution limit applies for employees aged 60, 61, 62, and 63who participate in 401(k)s and similar plans. For 2025, this higher catch-up contribution limit is $11,250 instead of $7,500.

Thus, people who turn those ages sometime during the year will be able to put up to $34,750 into their workplace retirement plans. That is about 14% more than in 2024 and marks the biggest change to 401(k) contribution rules in two decades.

The limits are the same if you choose pretax or Roth savings. Pretax contributions reduce your taxable income, the account grows tax-deferred, and you pay income tax on the principal and earnings when you eventually withdraw from the account.

With Roth accounts, you pay income tax upfront, the account grows tax-free, and withdrawals are generally tax-free. The Roth account must be opened for five years and you must be age 59½ or older to make tax-free withdrawals of earnings unless an IRS-approved exception applies.

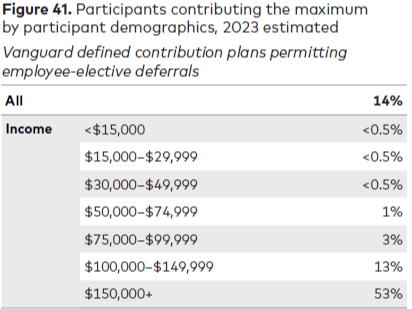

In Vanguard’s workplace retirement saving plans during 2023, 14% of participants saved the maximum, including catch-ups. Roughly two-thirds of participants with income over $100,000 contributed the maximum. Kudos to those participants for saving over 20% of their gross income for retirement! That’s a tall task, particularly on the heels of high inflation in 2021 and 2022.

Source: Vanguard. (2024). How America Saves.

The retirement law that created the super catch-up has a caveat: catch-up contributions must be Roth for those who earned more than $145,000 the previous year. That rule was supposed to go into effect in 2024, but the IRS has delayed it until 2026.

Unlike the 401(k) adjustments, the contribution limit for individual retirement accounts (IRAs) and Roth IRAs will remain the same in 2025 at $7,000, with a $1,000 catch-up for those 50 and older.

Our BCS Wealth Management team is here for you to navigate legislative changes pertaining to your investments. Don't hesitate to get in touch with us if you have questions.